First step into economics-hood

As I went through the excellent intro article, I can instinctively connect to some aspects of my personal life and to deeper insight into things. First of my newfound insights…

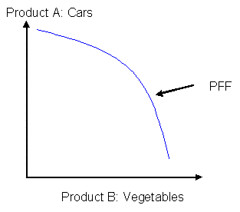

Businesses need to also compete across industries due to Production Possibility Frontier and opportunity cost. Production Possibility Frontier (PPF) is the point of most efficient production by a country. Let’s see an example of a country that produces only cars and vegetables. The curve shows the different production levels of cars vs vegetables when resources are allocated the best way possible. With current limits to production, the country needs to decide what combination of good and/or services (which point along the curve) is the best.

This makes me realise that industries are not independent of each other. As government policies favour one product, this implies a sidelining of another. All other factors being equal, if a government decides to increase production of cars, it is also forced to decrease production of vegetables. So, competition is not just between businesses within an industry but also across industries. Of course there are flaws to this theory

- The degree of cross industry competition may not be significant

- In the real world, other factors like means of production (technology, labour, etc) fluctuate as production of cars are increased, which may not actually lead to the need to decrease of vegetables production

Opportunity cost is the value foregone to have something else (quoting Investopedia). Example, I have $2. I can buy a cotton candy or an ice cream with this. If I’m an ice cream lover, then of course a $2 ice cream gives me more value than a $2 cotton candy. The value is personal to me.

If I choose to forego biscuit in favour of ice cream, then opportunity cost = cost of giving up biscuit (which is fine by me). But if for some reason I end up with the biscuit, then the opportunity cost = cost of giving up the ice cream (which is not desirable). By the way I love bittersweet chocolate ice cream.

If a country decides to produce more cars than vegetable to remain on the PFF curve, then opportunity cost equals the cost of giving up the required vegetable production.

If I was not deciding between food items but between ice cream and a comic book, don’t I then create a situation where Baskin & Robbins is competing with Marvel over my $2? Again it underlines the fact that products from different industries do need to compete to get the consumer’s bucks. This is especially true if these products are typically sold in an outlet, example – newspaper and sweets in a newsstand. Needless to say there’re also flaws to this understanding

- There’re not many situations where a comic book publisher need to compete with the ice cream manufacturer since different consumers will have different choices to make according to their taste. The said competition may be trivial since there’ll not be a critical mass of consumers that have to choose specifically between ice cream and a comic book.

But the fact that there is a clear relationship between products and goods across industries is made very clear. It intrigues me.

posted by Intrepid at 2:38 PM

![]()

![]()

0 Comments:

Post a Comment

<< Home